The landscape of health insurance underwent significant changes with the implementation of the Affordable Care Act (ACA), also known as Obamacare. A cornerstone of the ACA, effective from January 1, 2014, was the prohibition of insurers denying coverage or charging higher premiums based on pre-existing health conditions. This was achieved through guaranteed issue and modified community rating rules. Alongside tax credits designed to assist low and middle-income individuals in purchasing insurance through new health insurance marketplaces, these provisions aimed to broaden access to health coverage, especially for individuals with pre-existing conditions.

However, these reforms introduced potential challenges to the insurance market. Without additional regulatory mechanisms, insurers might be incentivized to avoid enrolling sicker individuals to maintain profitability, rather than focusing on offering the best value and quality of care to all consumers. Furthermore, the initial years of market reform brought uncertainty regarding pricing coverage for a newly expanded pool of enrollees, including those previously deemed “uninsurable,” which could lead to premium instability.

To address these potential market disruptions and foster a competitive environment based on quality and value, the ACA incorporated three key programs: risk adjustment, reinsurance, and risk corridors. These programs were specifically designed to stabilize the insurance market, particularly during the critical early years of the ACA’s implementation. This article will delve into the Affordable Care Act Risk Adjustment Program, its mechanics, purpose, and its role within the broader context of ACA market stabilization.

The Challenge of Adverse Selection and Risk Selection

To fully grasp the importance of the affordable care act risk adjustment program, it’s crucial to understand the concepts of adverse selection and risk selection in health insurance markets.

Adverse selection arises from the information asymmetry between insurers and consumers. Individuals with greater healthcare needs are inherently more likely to seek and purchase health insurance. This can lead to a situation where the insured pool disproportionately consists of higher-risk individuals. Consequently, the average cost of healthcare claims within the pool increases, potentially driving up premiums for everyone and destabilizing the insurance market. This can undermine the very goal of healthcare reform – to make insurance accessible and affordable for all. To mitigate adverse selection, the ACA implemented measures such as limiting open enrollment periods, mandating most individuals to have health coverage or face a penalty (the individual mandate, later repealed), and providing subsidies to help offset insurance costs.

Risk selection, on the other hand, is a strategic behavior by insurance companies. It occurs when insurers are incentivized to avoid enrolling individuals who are likely to incur high medical costs due to poorer health. While the ACA prohibits insurers from denying coverage or charging higher premiums based on health status, insurers can still employ subtle tactics to attract healthier, lower-cost individuals while discouraging enrollment from those with greater healthcare needs. This can be achieved through plan design, such as offering benefits packages or drug formularies that are less attractive to individuals with specific health conditions, or by promoting plan features like high deductibles and lower premiums that tend to appeal more to healthier individuals. Risk selection is detrimental to market efficiency because it shifts insurer competition away from improving service quality and value towards attracting a healthier clientele, ultimately not serving consumers’ best interests.

The affordable care act risk adjustment program, alongside reinsurance and risk corridors, was specifically created to counteract the potential negative consequences of both adverse selection and risk selection. These programs aimed to create a level playing field for insurers, encouraging them to compete on the basis of plan quality, efficiency, and value, rather than on their ability to cherry-pick healthier enrollees. Let’s examine the risk adjustment program in detail.

The Core Mechanism: Risk Adjustment

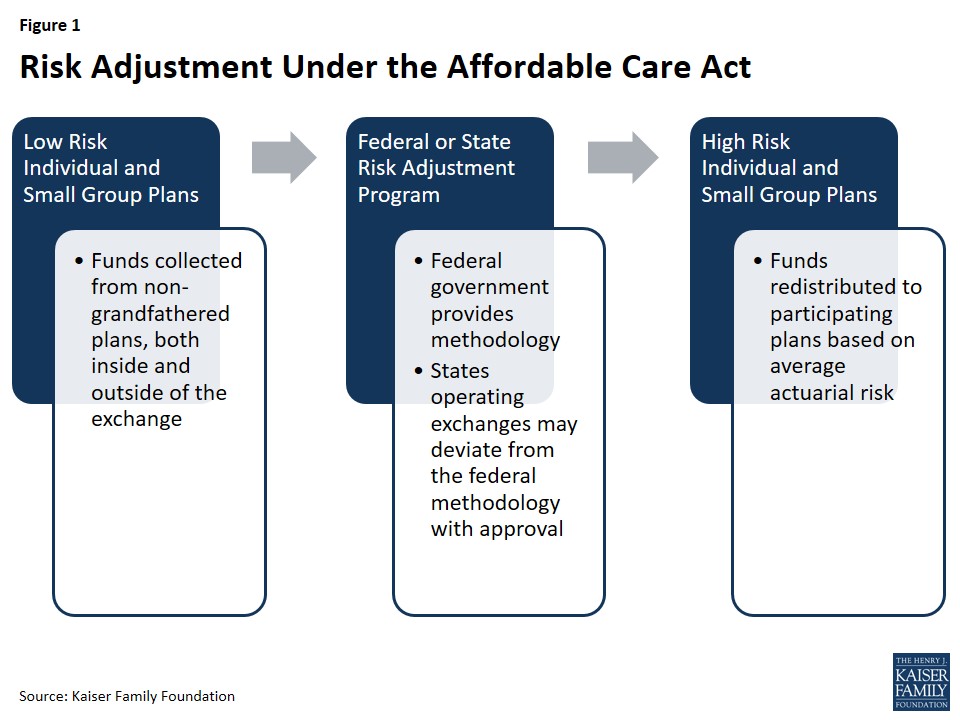

The affordable care act risk adjustment program serves as a critical mechanism to stabilize health insurance markets by directly addressing risk selection. Its fundamental purpose is to redistribute funds between insurance plans based on the health risk of their enrollees. Essentially, it transfers funds from plans with a predominantly healthy (lower-risk) enrollee population to plans that enroll a higher proportion of individuals with poorer health (higher-risk).

Figure 1: Visual representation of the Risk Adjustment program under the Affordable Care Act, illustrating the flow of funds from plans with lower-risk enrollees to plans with higher-risk enrollees.

By financially supporting plans that enroll higher-risk individuals, the affordable care act risk adjustment program reduces the financial incentive for insurers to engage in risk selection. This encourages them to compete on the merits of their plan offerings – the quality of care, the comprehensiveness of benefits, and the efficiency of service delivery – rather than trying to attract only the healthiest customers. Moreover, by mitigating risk selection, the program also contributes to premium stabilization within the health insurance marketplaces and helps control the cost of federal tax credit subsidies. If insurers outside the exchanges attempted to maintain artificially low premiums by steering sicker applicants towards exchange coverage, the risk adjustment program would counteract this by ensuring those plans enrolling sicker individuals within the exchange are adequately funded.

Program Participation: Who is Involved?

The affordable care act risk adjustment program has a broad reach, applying to all non-grandfathered plans operating in the individual and small group health insurance markets, both inside and outside of the health insurance exchanges (marketplaces). “Non-grandfathered” plans refer to those created or significantly altered after the ACA was enacted in March 2010. Plans existing prior to this date were “grandfathered” and are subject to fewer ACA regulations. However, these grandfathered plans lose their status if they undergo significant changes, such as substantial increases in cost-sharing or the imposition of new annual benefit limits. Plans renewed before January 1, 2014, and thus not fully subject to ACA requirements, are also excluded from the risk adjustment program. Notably, multi-state plans and Consumer Operated and Oriented Plans (CO-OPs) are included in the risk adjustment system. Unless a state chooses to merge its individual and small group markets, separate risk adjustment systems function independently within each market segment.

Government Oversight: Federal and State Roles

The oversight of the affordable care act risk adjustment program involves both federal and state governments, with the level of state involvement being optional. States that operate their own health insurance exchange have the choice to establish and run their own state-level risk adjustment program. Alternatively, they can opt to have the federal government administer the program within their state. States that do not operate their own exchange and instead utilize the federally-run exchange (the Health Insurance Marketplace) do not have the option to manage their own risk adjustment programs and must utilize the federal model. In states where the federal government (specifically, the Department of Health and Human Services – HHS) operates the risk adjustment program, insurers are charged a fee to cover the administrative costs of the program.

HHS has developed a federally-certified risk adjustment methodology that is available for states to use, or that HHS uses directly on behalf of states. States choosing to implement an alternative risk adjustment model must seek and obtain federal approval from HHS. Furthermore, these states are required to submit annual reports to HHS regarding their program operations. States electing to operate their own risk adjustment program are also mandated to publish a notice of benefit and payment parameters by March 1st of the year preceding the benefit year. Failure to do so means they forfeit the option to deviate from the federal methodology. Once a state’s alternative methodology receives federal certification, it becomes available for other states to adopt. Historically, Massachusetts was the only state to operate its own risk adjustment program but discontinued it in 2017. Since 2017, HHS has been responsible for operating the risk adjustment program in all states.

Calculating Payments and Charges: How Risk is Quantified

The core of the affordable care act risk adjustment program lies in its methodology for calculating payments and charges. This process hinges on assessing and comparing the average financial risk of enrollees across different insurance plans. The HHS methodology employs a sophisticated approach to estimate financial risk, utilizing enrollee demographics and medical claims data for specific diagnoses. It then compares plans within the same geographic area and market segment based on the average risk of their enrollees. This comparison determines which plans will be required to make payments into the system and which plans will receive payments.

The HHS methodology relies on the concept of individual risk scores. These scores are assigned to each enrollee based on their age, sex, and diagnosed medical conditions. Diagnoses are categorized into Hierarchical Condition Categories (HCCs), each assigned a numeric value reflecting the relative healthcare expenditures expected for an enrollee with that particular diagnosis. If an individual has multiple, unrelated diagnoses, the HCC values for each are incorporated into their individual risk score calculation. Additionally, for adult enrollees with specific combinations of illnesses (e.g., a severe illness and an opportunistic infection), an interaction factor is added to their risk score to account for the increased complexity and cost of care. Furthermore, an “induced utilization factor” is applied to the risk scores of enrollees receiving cost-sharing reductions under the ACA. This adjustment accounts for the potential increase in healthcare demand due to lower out-of-pocket costs, which is not otherwise captured by the other premium stabilization programs.

Once individual risk scores are calculated for all enrollees within a plan, these scores are averaged to determine the plan’s average risk score. This average risk score represents the plan’s predicted healthcare expenses. The HHS methodology also incorporates adjustments for factors like actuarial value (the level of patient cost-sharing within the plan), allowable rating variation, and geographic cost variations to ensure fair comparisons across different plan designs and locations. Under the risk adjustment mechanism, plans with a relatively low average risk score are required to make payments into the system, while plans with relatively high average risk scores receive payments.

These financial transfers (both payments and charges) are calculated by comparing each plan’s average risk score to a baseline premium, which is the average premium in the state. Calculations are performed separately for each geographic rating area, meaning insurers operating in multiple rating areas within a state will have multiple transfer amounts, which are then consolidated into a single invoice. Crucially, within each state, the total payments made into the risk adjustment system net to zero, meaning the program is designed to be budget-neutral within each state.

Recognizing the need for continuous improvement, CMS (Centers for Medicare & Medicaid Services) hosted a public conference in March 2016 and released a white paper to review the risk adjustment methodology and incorporate lessons learned from the initial years of program operation. The white paper explored potential refinements to the model, such as accounting for partial-year enrollees and prescription drug utilization. Subsequently, CMS proposed and implemented changes to incorporate partial-year enrollment in the 2017 benefit year and prescription drug utilization in the 2018 benefit year. Starting in 2017, preventive services were also integrated into the simulation of plan liability, and differentiated trend factors were introduced for traditional drugs, specialty drugs, and medical/surgical expenditures to better reflect the rising costs of prescription drugs. The risk adjustment model is periodically recalibrated using updated claims data, such as the Truven Health Analytics MarketScan Commercial Claims and Encounters database. In response to feedback from insurers during the initial years, CMS also began providing insurers with early estimates of their risk adjustment calculations to provide more timely information for premium setting. Furthermore, CMS has indicated ongoing exploration of modifications to the permanent risk adjustment program to better account for higher-cost enrollees, especially as the temporary reinsurance program concluded in 2016.

Data Collection and Privacy: Ensuring Accuracy and Confidentiality

Effective operation of the affordable care act risk adjustment program relies heavily on accurate and comprehensive data collection. However, this data collection must be balanced with the critical need to protect consumer privacy and confidentiality. Under the federal risk adjustment program, insurers are responsible for providing HHS with de-identified data, including enrollees’ individual risk scores. This ensures that sensitive personal information is not directly transmitted. While states operating their own programs are not mandated to use this specific data collection model, they are similarly restricted to collecting only the information reasonably necessary to operate the risk adjustment program and are explicitly prohibited from collecting personally identifiable information. Insurers are permitted to require healthcare providers and suppliers to submit the data necessary for risk adjustment calculations.

For each benefit year, insurers participating in the risk adjustment program (and reinsurance program) are required to establish a dedicated data environment, known as an EDGE server (External Data Gathering Environment). This secure server provides HHS with access to the necessary data within a specified timeframe. CMS has issued detailed guidance on EDGE server data submissions to ensure compliance.

To ensure data accuracy and program integrity, HHS recommends a two-tiered data validation process. Insurers are encouraged to first conduct an independent audit of their data before submitting it to HHS for a second audit. For the initial two benefit years (2014 and 2015), no payment adjustments were made as HHS focused on refining and optimizing the data validation process. However, starting in 2016, penalties for data submission failures or inaccuracies were implemented. Insurers failing to establish an EDGE server, submit required risk adjustment data, or found to have errors in their data through audits face adjustments to their average actuarial risk, impacting both payments and charges. Due to the multi-year nature of the audit process, the first payment adjustments (for the 2016 benefit year) were issued in 2018. Insurers failing to provide timely access to EDGE server data are assessed a default risk adjustment charge. Despite these stringent requirements, compliance has been high. In 2015, the vast majority of participating insurers successfully submitted the required EDGE server data, with only a small number being assessed the default charge.

Payments for Benefit Years 2014 and 2015: Initial Program Outcomes

The initial years of the affordable care act risk adjustment program demonstrated its operational effectiveness and financial impact. For the 2014 benefit year, HHS announced that $4.6 billion was transferred between insurers through the risk adjustment program, involving a total of 758 participating issuers. Independent analysis confirmed that the relative health of enrollees was the primary determinant of whether an insurer received a risk adjustment payment, indicating the program was functioning as intended by directing funds towards plans covering sicker populations. CMS reported this as a positive sign, confirming that the risk adjustment formula was effectively achieving its goal of transferring payments from plans with healthier enrollees to those with sicker enrollees.

For the 2015 benefit year, risk adjustment transfers averaged around 10% of premiums in the individual market and 6% in the small group market, consistent with the 2014 experience. Participation increased to 821 issuers. HHS provided each participating insurer with a detailed report outlining their specific risk adjustment payment or charge. It is important to note that risk adjustment payments for the 2015 benefit year were subject to sequestration at a rate of 7% due to government-wide spending cuts. However, HHS indicated that these sequestered funds were expected to become available for payment to insurers in the following fiscal year without further Congressional action.

Reinsurance and Risk Corridors: Complementary Programs

While the affordable care act risk adjustment program is a permanent feature of the ACA, it was complemented by two temporary programs – reinsurance and risk corridors – designed to provide additional market stabilization during the initial years of ACA implementation (2014-2016).

Reinsurance was a temporary program with the goal of further stabilizing individual market premiums during the early years of market reforms, particularly guaranteed issue. It operated by providing financial support to individual market insurance plans that enrolled high-cost individuals. This reduced the incentive for insurers to significantly increase premiums due to the new market rules guaranteeing coverage regardless of health status. Reinsurance differed from risk adjustment in its primary focus. Reinsurance aimed to stabilize premiums by mitigating concerns about higher-risk individuals enrolling early in the reformed market, whereas risk adjustment focused on mitigating risk selection among plans. Reinsurance payments were exclusively for individual market plans subject to the new market rules, while risk adjustment applied to both individual and small group plans. Furthermore, reinsurance payments were based on actual healthcare costs, whereas risk adjustment payments were based on predicted costs. Reinsurance also accounted for unexpectedly high costs even for low-risk individuals due to unforeseen events like accidents or sudden illnesses. Importantly, reinsurance represented a net inflow of funds into the individual market, effectively subsidizing premiums temporarily, unlike risk adjustment which is budget-neutral. Funding for reinsurance payments and program administration came from contributions collected from all health insurance issuers and third-party administrators across all market segments (individual, small group, and large group). HHS distributed reinsurance payments based on need, not proportionally to state contributions.

Figure 2: Visual representation of the Reinsurance program under the Affordable Care Act, showing the flow of funds to individual market plans with high-cost enrollees.

Risk Corridors was another temporary program designed to encourage insurers to participate in the exchanges and set accurate premiums in the early years (2014-2016). It aimed to protect insurers participating in the exchanges from extreme financial gains or losses during this period of market uncertainty. The risk corridors program established a target for exchange-participating insurers to spend 80% of premium revenue on healthcare and quality improvement. Insurers with costs significantly below this target (less than 97% of target) were required to make payments into the risk corridors program. These collected funds were then used to partially reimburse plans with costs exceeding the target (more than 103% of target). This program was intended to work in conjunction with the ACA’s Medical Loss Ratio (MLR) provision, which mandated insurers to spend at least 80% of premium dollars on medical care and quality improvement or issue refunds to enrollees. The risk corridors program was federally administered by HHS. However, subsequent congressional actions made the risk corridors program revenue-neutral, limiting payments to the amount collected from insurers, which ultimately resulted in significantly reduced payments to insurers and had a less stabilizing effect than initially intended.

Figure 3: Visual representation of the Risk Corridors program under the Affordable Care Act, illustrating the sharing of gains and losses between the government and Qualified Health Plans.

Conclusion: The Enduring Role of Risk Adjustment

The affordable care act risk adjustment program, alongside the temporary reinsurance and risk corridors programs, was a crucial set of mechanisms within the ACA designed to foster a stable and competitive health insurance market. While reinsurance and risk corridors were time-limited programs intended for the initial years of market reform, the risk adjustment program is a permanent feature, playing a vital long-term role in mitigating risk selection and promoting fair competition among insurers. These programs were designed to be complementary, with many health insurance plans being subject to more than one. Specifically, risk adjustment is designed to counter incentives for plans to attract healthier individuals and to compensate plans that enroll a disproportionately sick population. Risk corridors were intended to reduce overall financial uncertainty for insurers in the exchanges, although their effectiveness was limited by funding constraints. Reinsurance provided direct financial support to plans covering high-cost enrollees and, through its funding mechanism, provided a general subsidy to individual market premiums for its three-year duration. The expiration of the reinsurance program is expected to contribute to higher premium increases in subsequent years, highlighting the ongoing and critical importance of the affordable care act risk adjustment program in maintaining a stable and accessible health insurance market under the ACA.