The Affordable Care Act (ACA), enacted in 2010, brought about significant changes to the health insurance landscape in the United States. A cornerstone of this legislation was the mandate that insurers could no longer deny coverage or charge higher premiums based on pre-existing health conditions. This provision, known as guaranteed issue and modified community rating, aimed to make health insurance more accessible, particularly for individuals with chronic illnesses. Coupled with tax credits to help low- and middle-income individuals purchase insurance through new health insurance marketplaces, the ACA sought to dramatically expand coverage.

However, these reforms introduced potential challenges to the insurance market. Without careful regulatory oversight, insurers might be incentivized to avoid enrolling sicker individuals, a practice known as risk selection, instead of focusing on providing better value and quality care to all consumers. Furthermore, the initial years of market reform were marked by uncertainty for insurers as they navigated pricing coverage for a newly expanded pool of enrollees, including those previously considered “uninsurable.” This uncertainty could lead to premium instability and market disruption.

To address these potential issues and foster a stable, competitive health insurance market, the ACA included several key provisions. Among these were three temporary programs—reinsurance and risk corridors—and one permanent program: risk adjustment. These programs were designed to encourage insurers to compete on the basis of quality and efficiency, rather than by avoiding high-risk individuals, and to stabilize premiums, especially during the critical early years of the ACA’s implementation. This article will delve into these programs, with a particular focus on the Affordable Care Act’s risk adjustment program, exploring its mechanics, goals, and impact on the health insurance market.

The Challenge of Adverse Selection and Risk Selection

To fully appreciate the role of the ACA’s risk adjustment program, it’s essential to understand the concepts of adverse selection and risk selection in the context of health insurance.

Adverse selection arises from the information asymmetry between insurers and consumers. Individuals with a greater need for healthcare are more likely to seek and purchase health insurance. If insurers are unable to accurately assess and price for this varying risk, it can lead to a situation where the insurance pool becomes disproportionately composed of high-risk individuals. This, in turn, drives up average premiums, potentially making insurance less affordable for everyone, including healthier individuals who might then opt out, further destabilizing the market. To mitigate adverse selection, the ACA implemented measures like limited open enrollment periods, individual mandates (initially with a penalty for non-compliance), and subsidies to assist with insurance costs, encouraging broad participation and discouraging individuals from waiting until they are sick to purchase coverage.

Risk selection, on the other hand, is a strategy employed by insurers. It occurs when insurance companies have an incentive to avoid enrolling individuals who are likely to be high-cost, meaning those with poorer health and greater anticipated medical needs. While the ACA prohibits denying coverage or charging higher premiums based on health status, insurers might still attempt to attract healthier clients through various means. This could involve designing plans with benefit structures, cost-sharing arrangements (like deductibles and co-pays), or drug formularies that are less appealing to individuals with chronic conditions. For example, a plan with a very high deductible and low premium might be more attractive to a healthy person who anticipates minimal healthcare utilization but less so for someone managing a chronic illness.

This type of risk selection is problematic because it shifts the focus of competition away from providing value and quality to consumers and towards attracting a healthier, and thus cheaper, risk pool. Such competition undermines the goals of a stable and equitable health insurance market.

The ACA’s risk adjustment, reinsurance, and risk corridors programs were specifically designed to counteract the potentially detrimental effects of both adverse selection and risk selection. These programs aimed to create a level playing field for insurers, encouraging them to compete on quality and efficiency rather than on their ability to cherry-pick healthy enrollees. They also played a crucial role in stabilizing premiums, particularly in the nascent years of the ACA marketplaces.

The following table summarizes the key characteristics of these three programs:

| Table 1: Summary of Risk and Market Stabilization Programs in the Affordable Care Act |

|---|

| Risk Adjustment |

| What the program does |

| Whyit was enacted |

| Who participates |

| How it works |

| Whenit goes into effect |

Deep Dive into the Affordable Care Act’s Risk Adjustment Program

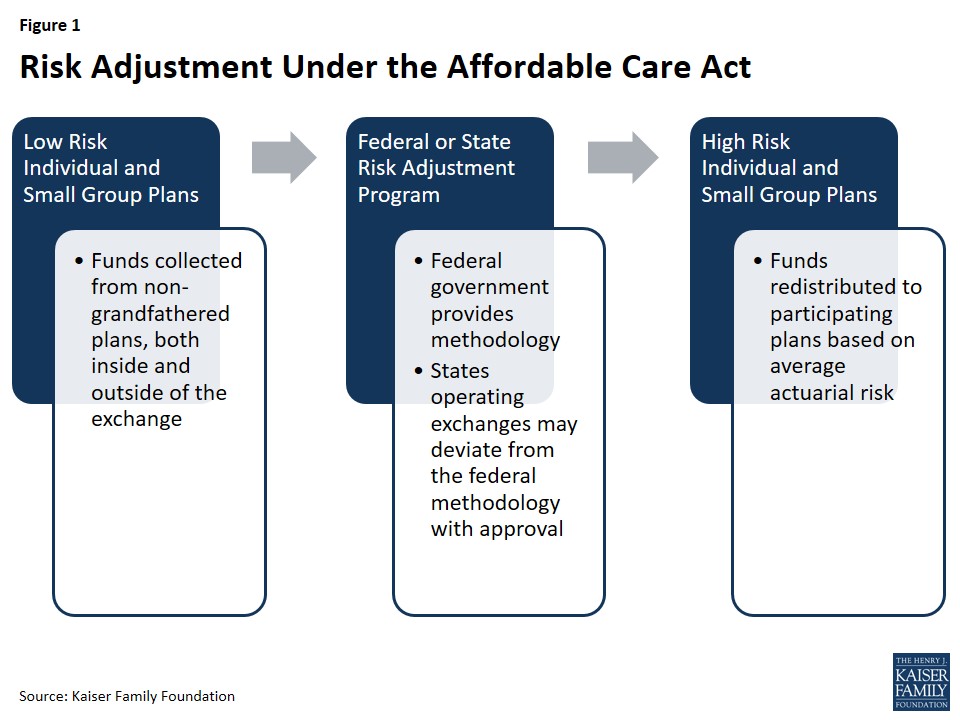

The Affordable Care Act’s risk adjustment program stands as a permanent mechanism to counteract risk selection and foster fair competition among insurers. It operates by transferring funds from health insurance plans with a predominantly healthy enrollee population to plans that cover a higher proportion of individuals with greater healthcare needs. This financial redistribution is crucial for several reasons.

Firstly, it directly addresses the incentive for insurers to engage in risk selection. By mitigating the financial advantage of attracting only healthy individuals, the risk adjustment program encourages insurers to compete on the basis of plan quality, benefit design, and the efficiency of care delivery. Insurers are incentivized to provide better value to all consumers, including those with chronic conditions, rather than trying to avoid them.

Secondly, the risk adjustment program contributes to premium stabilization, both within and outside of the health insurance marketplaces. If insurers operating outside the exchanges were to aggressively attract healthy individuals to keep their premiums artificially low, while sicker individuals disproportionately enrolled in exchange plans, it could lead to instability in the exchanges and increased costs for government subsidies designed to make exchange coverage affordable. Risk adjustment helps to level the playing field across the entire individual and small group markets, regardless of whether plans are sold inside or outside the exchanges.

Figure 1: Risk Adjustment Under the Affordable Care Act

Program Participation: Who is Involved?

The risk adjustment program has a broad reach, encompassing non-grandfathered health insurance plans in both the individual and small group markets. This includes plans offered both within and outside of the ACA marketplaces or exchanges. “Non-grandfathered” plans refer to those created or significantly altered after the ACA was enacted in March 2010. Grandfathered plans, those existing prior to the ACA’s passage and maintaining their basic structure, are exempt from many ACA requirements, including risk adjustment. However, if a grandfathered plan makes substantial changes, such as significantly increasing cost-sharing or imposing new annual benefit limits, it can lose its grandfathered status and become subject to risk adjustment.

Plans renewed before January 1, 2014, and thus not fully subject to ACA rules, are also excluded from risk adjustment. However, multi-state plans and Consumer Operated and Oriented Plans (CO-OPs), which were created under the ACA to foster competition, are participants in the risk adjustment program. Unless a state chooses to merge its individual and small group markets, separate risk adjustment systems operate within each market segment.

Government Oversight: Federal and State Roles

The administration of the risk adjustment program involves both federal and state governments. States that operate their own health insurance exchanges have the option to establish and run their own state-level risk adjustment programs. Alternatively, they can defer to the federal government to administer the program within their state. States that do not operate their own exchange and instead utilize the federally-run exchange (Health Insurance Marketplace) are required to use the federal risk adjustment model. In states where the federal government (specifically, the Department of Health and Human Services or HHS) administers risk adjustment, insurers are charged a fee to cover the administrative costs of the program.

HHS has developed a federally-certified risk adjustment methodology that can be adopted by states or used by HHS on behalf of states. States wishing to implement an alternative risk adjustment model must seek federal approval and submit annual reports to HHS detailing their program’s operation. States choosing to run their own programs are also required to publish notices of benefit and payment parameters by March 1st of the year preceding the benefit year; failure to do so means they must adhere to the federal methodology. Once a state’s alternative methodology is approved by HHS, it becomes federally-certified and can potentially be adopted by other states. Massachusetts was the only state to initially operate its own risk adjustment program but discontinued it in 2017. Since 2017, HHS has been responsible for operating risk adjustment programs in all states.

Calculation of Payments and Charges: How Risk is Assessed

At the heart of the risk adjustment program is the methodology for calculating payments and charges. The program compares eligible insurers based on the average actuarial risk of their enrollees. The HHS methodology uses a sophisticated approach to estimate financial risk, taking into account enrollee demographics and claims data for specific medical diagnoses. It then compares plans within the same geographic area and market segment based on the average risk of their enrolled populations to determine which plans will make payments and which will receive them.

The HHS methodology assigns individual risk scores to each enrollee. These scores are based on factors like age, sex, and medical diagnoses. Diagnoses are categorized into Hierarchical Condition Categories (HCCs), each assigned a numeric value reflecting the relative expected healthcare expenditures for an enrollee with that diagnosis. If an individual has multiple, unrelated diagnoses, the HCC values for each are factored into their individual risk score. Furthermore, interaction factors are added for enrollees with certain combinations of illnesses, such as a severe illness and an opportunistic infection, to account for the potentially higher costs associated with complex health conditions.

For enrollees receiving cost-sharing reductions under the ACA (which lower out-of-pocket costs for eligible individuals), an induced utilization factor is applied. This adjustment acknowledges that lower cost-sharing may lead to increased demand for healthcare services, which is not otherwise captured by the risk adjustment model.

Once individual risk scores are calculated for all enrollees in a plan, these scores are averaged to arrive at the plan’s average risk score. This average risk score represents the plan’s predicted expenses, reflecting the overall health risk of its enrollee population. The HHS methodology also incorporates adjustments for factors like actuarial value (the percentage of healthcare costs covered by the plan), allowable rating variation, and geographic cost differences to ensure fair comparisons between plans.

Under the risk adjustment system, plans with a relatively low average risk score, indicating a healthier enrollee population, make payments into the system. Conversely, plans with a relatively high average risk score, reflecting a sicker enrollee population, receive payments. These transfers are calculated by comparing each plan’s average risk score to a baseline premium, which is the average premium in the state. Calculations are performed for each geographic rating area within a state, and insurers operating in multiple rating areas receive a consolidated invoice reflecting their total transfer amounts. Crucially, within a given state and market (individual or small group), the total payments made by plans equal the total payments received, ensuring the program is budget-neutral.

CMS (Centers for Medicare & Medicaid Services) has continued to refine the risk adjustment methodology over time, incorporating new data and addressing emerging issues. For instance, CMS has explored and implemented adjustments to account for partial-year enrollees and prescription drug utilization to further enhance the accuracy and effectiveness of the risk adjustment model. They also provide insurers with early estimates of risk adjustment calculations to aid in premium setting and improve market predictability. As the temporary reinsurance program concluded in 2016, CMS has also been exploring modifications to the permanent risk adjustment program to better address the needs of plans with exceptionally high-cost enrollees.

Data Collection and Privacy: Protecting Enrollee Information

Data collection is a critical component of the risk adjustment program. To protect consumer privacy and confidentiality, the federal risk adjustment program mandates that insurers provide HHS with de-identified data, including enrollees’ individual risk scores. While states operating their own programs are not required to use this specific data collection model, they are similarly obligated to collect only the data necessary for program operation and are prohibited from collecting personally identifiable information. Insurers are permitted to require healthcare providers and suppliers to submit the data needed for risk adjustment calculations.

For each benefit year, insurers participating in risk adjustment are required to establish a dedicated data environment, known as an EDGE server (External Data Gathering Environment), and provide HHS with data access within a specified timeframe. This EDGE server system facilitates secure data submission and processing. CMS has issued detailed guidance on EDGE data submissions to ensure data quality and consistency.

To further ensure data accuracy, HHS recommends that insurers conduct independent audits of their data before submitting it to HHS for a secondary audit. Initially, for the 2014 and 2015 benefit years, no payment adjustments were made as HHS focused on optimizing the data validation process. However, starting in 2016, penalties were introduced for data submission failures or inaccuracies. Insurers failing to establish an EDGE server, submit risk adjustment data, or with identified data errors face adjustments to their average actuarial risk, and consequently, to their payments or charges. Due to the audit process timeline, payment adjustments for a given benefit year are typically issued in the subsequent year. Insurers failing to provide timely EDGE server data access are assessed a default risk adjustment charge. Despite these requirements, compliance has been high, with the vast majority of participating insurers successfully submitting the necessary data.

Payments for Benefit Years 2014 and 2015: Initial Program Results

The initial years of the risk adjustment program demonstrated its significant financial impact on the health insurance market. For the 2014 benefit year, approximately $4.6 billion was transferred between insurers through the risk adjustment program, with 758 insurers participating. Independent analyses indicated that the relative health of an insurer’s enrollees was the primary factor determining whether they received a risk adjustment payment, suggesting the program was functioning as intended – directing funds from plans with healthier enrollees to those with sicker enrollees. CMS has cited these results as evidence that the risk adjustment formula effectively promotes a more level playing field.

For the 2015 benefit year, risk adjustment transfers averaged around 10% of premiums in the individual market and 6% in the small group market, similar to the 2014 experience. 821 insurers participated in the program in 2015. HHS provided each participating insurer with a report detailing their specific risk adjustment payment or charge.

It’s important to note that risk adjustment payments for the 2015 benefit year were subject to sequestration at a rate of 7%, due to government-wide spending cuts. However, HHS indicated that these sequestered funds were expected to become available for payment to insurers in the following fiscal year without further Congressional action.

Reinsurance: A Temporary Premium Stabilizer

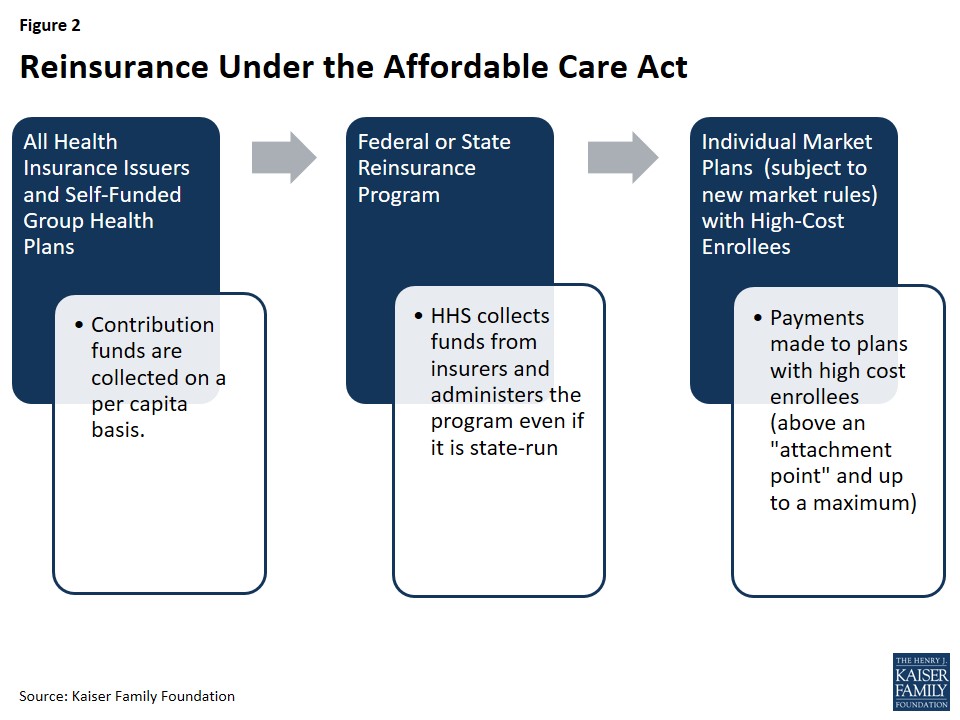

Alongside risk adjustment, the ACA included a temporary reinsurance program, active from 2014 through 2016. The primary goal of reinsurance was to further stabilize premiums in the individual market during the initial years of market reforms, particularly guaranteed issue. Reinsurance aimed to reduce the risk for insurers associated with enrolling individuals with pre-existing conditions by partially offsetting the costs of unexpectedly high claims.

Reinsurance differs from risk adjustment in its purpose and mechanics. While risk adjustment is a permanent program designed to mitigate risk selection across plans, reinsurance was a temporary measure to address broader premium instability in the early years of market reform. Reinsurance focused on reducing the incentive for insurers to set high premiums due to uncertainty about the health risk of new enrollees, whereas risk adjustment focuses on ensuring fair compensation based on the actual risk profile of enrolled populations.

Reinsurance payments were made only to individual market plans subject to the ACA’s new market rules, while risk adjustment applies to both individual and small group plans. Furthermore, reinsurance payments were based on actual healthcare costs incurred, whereas risk adjustment payments are based on predicted costs derived from risk scores. This meant reinsurance could also provide support for plans that unexpectedly incurred high costs even for low-risk individuals, such as in cases of accidents or sudden illnesses. A plan could potentially receive both reinsurance and risk adjustment payments for the same high-cost enrollee.

Unlike risk adjustment, which is budget-neutral within each market, reinsurance involved a net inflow of funds into the individual market, effectively subsidizing premiums for a limited time. These funds were collected from all health insurance issuers and third-party administrators across all market segments (individual, small group, and large group). HHS distributed reinsurance payments based on need, not proportionally to state contributions, aiming to efficiently target funds to where they were most needed to stabilize individual market premiums nationwide.

Figure 2: Reinsurance Under the Affordable Care Act

Program Participation: Broad Contribution, Targeted Benefit

The reinsurance program had a broad base of financial support. All issuers of fully-insured major medical products in the individual, small group, and large group markets, as well as self-funded plans, were required to contribute funds to the reinsurance program. However, reinsurance payments were specifically directed to individual market issuers covering high-cost individuals and complying with the ACA’s market rules. State high-risk pools, which predated the ACA and served as coverage options for individuals with pre-existing conditions, were excluded from the reinsurance program.

Government Oversight: Predominantly Federal

While states had the option to operate their own reinsurance programs, the federal government played a significant oversight role. For states choosing to run their own programs, there was no formal HHS approval process, but their flexibility to deviate from federal guidelines was limited. HHS collected all reinsurance contributions, even for state-run programs, and all states were required to adhere to a national payment schedule. States wishing to modify data requirements needed to publish notices of benefit and payment parameters. States could choose to collect additional funds beyond the national level if they anticipated higher reinsurance payment needs or administrative costs. States were permitted to continue reinsurance programs beyond 2016, but they could not utilize funds collected under the ACA’s reinsurance program after 2018. Connecticut was the only state to operate its own reinsurance program for the 2014 and 2015 benefit years. Alaska implemented a two-year reinsurance program in 2016, effectively repurposing its previous high-risk pool as a reinsurance fund, covering claims for the 2015 and 2016 benefit years.

Calculation of Payments and Charges: Attachment Points and Caps

The ACA established national funding levels for the reinsurance program: $10 billion in 2014, $6 billion in 2015, and $4 billion in 2016. Based on enrollment estimates, HHS set a uniform reinsurance contribution rate per person: $63 in 2014, $44 in 2015, and $27 in 2016.

Reinsurance payments were triggered when an individual enrollee’s healthcare costs exceeded a certain threshold, known as the attachment point. HHS set the attachment point at $45,000 for 2014 and 2015. Due to the reduced reinsurance funding pool in 2016, the attachment point was raised to $90,000 for that year. Additionally, a reinsurance cap, set at $250,000 for all three years, defined the maximum cost eligible for reinsurance per enrollee.

The coinsurance rate determined the percentage of costs between the attachment point and the reinsurance cap that would be reimbursed through the program. Initially, this rate was set at 80% in 2014 and 50% in 2015 and 2016. If reinsurance contributions exceeded payment requests, the coinsurance rate could be increased, up to a maximum of 100%. For example, in 2014, due to higher than anticipated contributions, HHS was able to reimburse 100% of eligible claims instead of the initial 80%. In 2015, the coinsurance rate was increased to 55.1%. Surplus reinsurance funds could be rolled forward to subsequent benefit years. Conversely, if contributions fell short of payment requests, payments would be reduced proportionately. The total payments were capped by the total amount collected in contributions.

States opting to supplement federal reinsurance could do so by adjusting program parameters like the attachment point, reinsurance cap, and coinsurance rate, but only in ways that increased, not decreased, reinsurance payments.

Data Collection and Privacy: Utilizing EDGE Servers

Reinsurance payments were based on medical cost data to identify high-cost enrollees. Therefore, data collection was essential for program operation. HHS, or state reinsurance entities, required access to claims data and data on cost-sharing reductions to accurately calculate payments. In states where HHS administered reinsurance, they utilized the same secure EDGE server system as the risk adjustment program for data collection, ensuring data privacy and limiting the collection of personally identifiable information to what was strictly necessary for payment calculations. HHS also proposed conducting audits of participating insurers and state-run programs to ensure data integrity.

Similar to risk adjustment, no payment adjustments were made for the 2014 and 2015 reinsurance years as data validation processes were refined. However, starting in 2016, insurers failing to establish an EDGE server or meet data submission requirements risked forfeiting reinsurance payments. Compliance with data submission requirements was also high in the reinsurance program.

Payments for Benefit Years 2014 and 2015: Program Impact

The reinsurance program played a significant role in the early years of the ACA marketplaces. For the 2014 benefit year, reinsurance contributions ($9.7 billion) exceeded payment requests ($7.9 billion), allowing CMS to pay out 100% of eligible claims, totaling $7.9 billion to 437 insurers nationwide. The surplus of $1.7 billion was rolled over to the 2015 benefit year.

This surplus, combined with 2015 contributions, allowed CMS to make an early partial reinsurance payment in March and April 2016, based on a 25% coinsurance rate. For the full 2015 benefit year, estimated reinsurance contributions ($6.5 billion) were less than payment requests ($14.3 billion). CMS estimated it would make approximately $7.8 billion in payments to 497 insurers at a coinsurance rate of 55.1%. This payment amount was supported by the carried-over surplus from 2014 and additional 2015 contributions.

Reinsurance payments for the 2015 benefit year were also subject to sequestration at a rate of 6.8%. Despite this, the reinsurance program provided substantial financial support to insurers in the individual market during its three-year lifespan, contributing to premium stability and mitigating the initial risks associated with market reforms. An analysis by CMS based on reinsurance payments suggested that per-enrollee costs in the individual market remained relatively stable between 2014 and 2015, potentially indicating the program’s effectiveness in managing cost pressures.

Risk Corridors: Sharing Gains and Losses

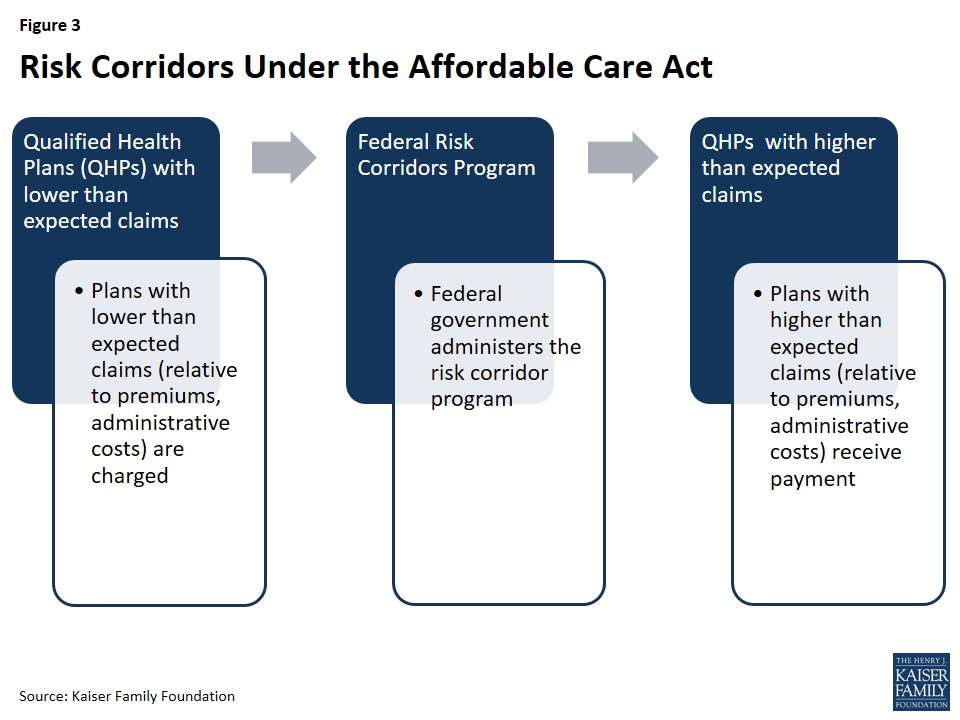

The third temporary premium stabilization program under the ACA was risk corridors, also active from 2014 through 2016. Risk corridors were designed to encourage insurers to participate in the new health insurance exchanges by mitigating the financial uncertainty associated with setting premiums in a new market. The program aimed to protect insurers from extreme financial gains or losses during the initial years of exchange operation.

Figure 3: Risk Corridors Under the Affordable Care Act

The risk corridors program set a target for exchange-participating insurers to spend 80% of premium revenue on healthcare and quality improvement. Insurers with costs significantly lower than this target were required to make payments into the risk corridors program, while those with costs significantly higher received payments. This mechanism was intended to share risk between insurers and the government during the initial period of market instability.

The risk corridors program was designed to complement the ACA’s medical loss ratio (MLR) provision, which requires most individual and small group insurers to spend at least 80% of premium dollars on medical care and quality improvement, or else issue rebates to enrollees.

Program Participation: Qualified Health Plans

Participation in the risk corridors program was limited to Qualified Health Plans (QHPs), which are plans certified to be offered on the health insurance exchanges. QHPs offered both inside and outside of the exchanges were subject to risk corridors. Only plans with costs falling outside of a defined range around their target spending level were required to make payments or were eligible to receive payments.

Government Oversight: Federal Administration

The risk corridors program was administered solely by the federal government. HHS collected funds from plans with lower-than-expected claims and disbursed payments to plans with higher-than-expected claims, acting as a central risk-sharing entity.

Calculation of Payments and Charges: Target Amounts and Allowable Costs

Each year, each QHP was assigned a target amount for allowable costs, which included expenditures on enrollee medical care and quality improvement activities, consistent with the ACA’s MLR calculations. Insurers were required to reduce their allowable costs by any cost-sharing reduction payments received from HHS.

The risk corridor program established thresholds around this target amount. If an insurer’s actual claims fell within plus or minus 3% of their target amount, they neither paid into nor received payments from the risk corridors program – they bore the full financial risk or benefit. However, QHPs with lower-than-expected claims paid into the program on a sliding scale:

- For claims falling 3% to 8% below the target, the insurer paid 50% of the difference between actual claims and 97% of the target amount.

- For claims falling more than 8% below the target, the insurer paid 2.5% of the target amount plus 80% of the difference between actual claims and 92% of the target.

Conversely, QHPs with higher-than-expected costs received payments from the program:

- For claims exceeding the target amount by 3% to 8%, the insurer received 50% of the amount exceeding 103% of the target.

- For claims exceeding the target amount by more than 8%, the insurer received 2.5% of the target amount plus 80% of the amount exceeding 108% of the target.

In response to concerns about individual market plan cancellations in 2013, HHS implemented a transitional policy allowing certain plans to be reinstated. To account for the potential impact of this policy change on the exchange risk pool, HHS modified the risk corridors program in 2015, adjusting the calculation of allowable costs by increasing the ceiling on administrative costs and the profit margin floor by 2%.

Initially, the ACA statute did not mandate that risk corridor payments be budget-neutral. However, subsequent appropriations bills in 2015 and 2016 stipulated that risk corridor payments could not exceed collections, and CMS was prohibited from using funds from other accounts to cover risk corridor payments. This effectively made the program revenue-neutral. In years where claims exceeded collections, payments were reduced proportionally, and any outstanding claims were carried over to be paid from future collections. If the three-year program ended with unpaid claims, HHS indicated it would seek Congressional funding, subject to appropriations.

Data Collection and Privacy: Leveraging MLR Data

To calculate risk corridor payments and charges, QHPs were required to submit financial data to HHS, including premiums earned and cost-sharing reduction payments received. To streamline data collection, HHS aligned the data requirements and validation processes for risk corridors with those of the ACA’s Medical Loss Ratio (MLR) provision, minimizing administrative burden for insurers. Audits for the risk corridors program were also coordinated with audits for reinsurance and risk adjustment to further reduce insurer burden.

Payments for Benefit Year 2014: Significant Shortfall

For the 2014 benefit year, risk corridor claims significantly exceeded contributions. Total claims amounted to $2.87 billion, while insurer contributions totaled only $362 million. As a result, risk corridor payments for 2014 claims were made at a rate of only 12.6% of the promised amount. CMS anticipated that remaining 2014 claims would be paid from 2015 collections, and any 2015 shortfalls would be covered by 2016 collections. However, due to the revenue-neutrality requirement imposed by Congress, it became clear that the risk corridors program would not fully compensate insurers for their losses. This shortfall created financial challenges for some insurers participating in the exchanges and contributed to market instability in some areas.

Conclusion: A Multifaceted Approach to Market Stability

The Affordable Care Act’s risk adjustment, reinsurance, and risk corridors programs represented a comprehensive strategy to address potential market disruptions arising from the ACA’s reforms. These programs were designed to work in concert to mitigate adverse selection and risk selection, and to foster a more stable and competitive health insurance market, particularly in the initial years of implementation. While reinsurance and risk corridors were temporary measures, the risk adjustment program is a permanent feature of the ACA, continuing to play a vital role in the individual and small group health insurance markets.

While all three programs shared the overarching goal of premium stabilization, they operated through distinct mechanisms and targeted different aspects of market risk. Risk adjustment is specifically designed to counteract incentives for risk selection, ensuring that insurers are fairly compensated for enrolling higher-risk individuals and are not penalized for doing so. Risk corridors, despite facing funding limitations, were intended to reduce overall financial uncertainty for insurers in the exchanges during the initial years. Reinsurance provided direct financial support to plans covering high-cost enrollees, effectively subsidizing individual market premiums for a limited period.

The expiration of the temporary reinsurance program at the end of 2016 was expected to contribute to premium increases in subsequent years, highlighting the significant role it played in initial premium stabilization. The Affordable Care Act’s risk adjustment program, however, remains a critical, ongoing mechanism for promoting a more equitable and sustainable health insurance market by mitigating risk selection and encouraging competition based on value and quality, ultimately benefiting consumers.